Archive : Article / Volume 1, Issue 2

- Research Article | DOI:

- https://doi.org/10.58489/2836-2179/009

Balanced Scorecard applied to Hospital Units - a systematic review of the literature

PhD student at the School of Economics and Management of Minho University, and is a professor of Accounting and Management.

Paula Cristina de Almeida Marques

Paula C. de A. Marques, (2022). Balanced Scorecard applied to Hospital Units - a systematic review of the literature. Journal of Emergency and Nursing Management. 1(2). DOI: 10.58489/2836-2179/009

© 2022 Paula C. de A. Marques, this is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

- Received Date: 13-10-2022

- Accepted Date: 24-10-2022

- Published Date: 29-12-2022

BSC, Health, Hospital, Performance Evaluation

Abstract

As a result of the reality currently experienced in the health sector, where there is an increase in competitiveness and where cost control is increasingly evident, performance management in this area is distinct and more complex, compared to other areas. Thus, the Balanced Scorecard (BSC) emerged as the ideal tool to improve the performance of healthcare organizations.

The BSC is a management tool with the potential to clarify the strategic objectives of health organizations and to assist in the selection of the most appropriate performance indicators to use. For its success, it is important to align the organization's strategy with the services' strategy, as well as the involvement of managers.

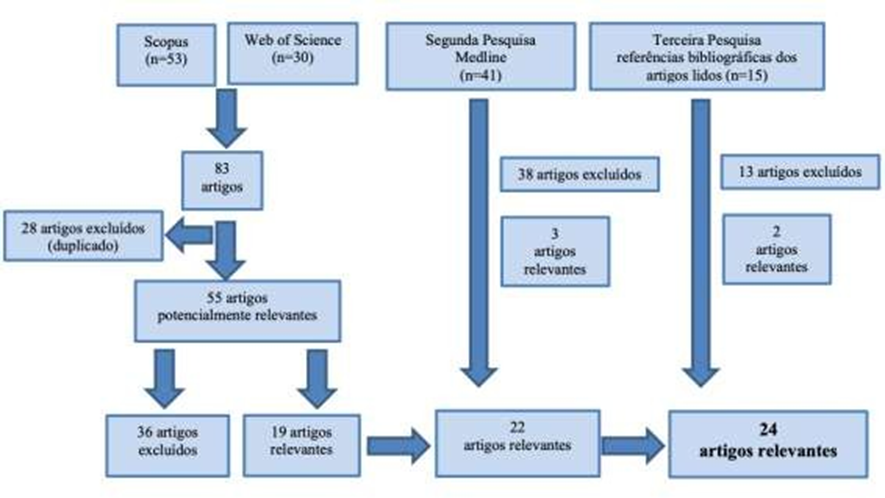

This investigation has as main objective to make a diagnosis of the state of the art, regarding the implementation of the BSC in Hospital Units. To achieve this objective, a systematic review of the literature was carried out and nine questions related to the objective in question were answered.

From the investigation carried out, 24 articles were selected for the literature review, which met the inclusion criteria. From the analysis of these articles, it was possible to conclude that the implementation of this tool can represent an added value for the success of health organizations in general, and of Hospital Units in particular. Empirical evidence suggests that, through the implementation of the BSC, Hospital Units have managed to increase their level of quality, the satisfaction of users and professionals, as well as contributing to their efficiency and effectiveness. However, and despite its benefits, the implementation of the BSC is still not a linear process, with several limitations and/or difficulties being identified in the design and implementation process of this tool.

Conclusion

With this systematic literature review, our objective was to explore and understand the state of the art on BSC in Hospital Units. This tool is increasingly important in the health sector and, as such, it is pertinent to understand what had already been studied, thus allowing a better understanding of the subject.

The BSC is a management tool that initially appeared in 1992, by the hands of Kaplan and Norton, aimed at the private sector; only later did it gain relevance within health organizations and in the public sector. It is currently considered a very useful tool in the private sector, in the public sector, in the public-private sector and in the social sector. Traditionally made up of four perspectives, with the advancement of knowledge about this tool, it has already been possible to find new perspectives, which reflect, on the one hand, the need for organizations to move towards efficiency and, on the other hand, the permeability/flexibility of the BSC. to the needs of organizations. Regarding the indicators outlined for each perspective, they vary greatly from application to application, however,

Although all publications mention the importance that this tool assumes in the field of health, there are still many gaps in terms of its implementation. Kompouros (2013) points out as one of these gaps the reluctance to change, which, in many cases, can be due to the lack of knowledge about the BSC, the lack of a quality culture within organizations (El-Jardali et al., 2011) or the inability of leadership to communicate the purpose of implementing the BSC (Rabbani et al., 2011). It is thus clear that it is extremely important to create specific teams for the implementation of this tool, and that they are in the field, monitoring and evaluating the work developed, transmitting the feedback to the service, department and/or hospital institution and making adjustments as necessary.

Although not all the analysed publications specify the benefits achieved with the implementation of the BSC, those that do point to an increase in the satisfaction of users and professionals, an increase in quality and efficiency. The analysed literature is consensual, with regard to the main motivation for the implementation of the BSC, recognizing its potential as a driver for the improvement of care provided, as a performance evaluation system.

With the answer to each of the questions initially raised, we can reach some conclusions, which we refer to in the next paragraphs.

Most of the studies found were carried out in the last decade, they are mostly qualitative and were published in reputable magazines and newspapers in this area. Overall, these studies aimed to better understand the BSC tool and clarify its impact on improving the performance of Hospital Units.

Regarding the main motivation pointed out by the researchers for carrying out the study, those most frequently mentioned are related to the need to develop a performance evaluation system for Hospital Units and to deepen knowledge and empirical research on the application of this tool.

According to the publications analysed, the Public Sector Hospital Units are the ones where the BSC was most applied. With regard to geographic distribution, most studies were carried out in Asia and North America, with only four studies being identified in Europe.

Also, according to the reports found, it appears that during the design and implementation of the BSC, top management and direction, health professionals, reference professionals from each sector where the BSC is intended to be implemented, a panel of experts must be involved. in this tool, users and academics.

With regard to perspectives, the most frequently used is the financial perspective that takes the lead. Although most studies use the perspectives of the Kaplan and Norton model, some studies adapt them, and there are even studies that create new perspectives, it seems to us that this innovation is closely associated with the need to adapt to the reality of each organization. With regard to indicators, from the Customers perspective, the most used indicators are those related to the satisfaction rate: from the financial perspective, the most used are related to costs and expenses, margin and level revenue; from the Internal Processes perspective, the most used indicators are those related to the time factor, satisfaction, professional incidents and occupation, finally, from the Learning and Knowledge perspective, there is a large reference to indicators related to training and research, investment in technology and the environment organizational.

Regarding the elements pointed out as facilitators in the different publications, it is clear that open communication, the dissemination of results and the involvement of top managers contribute to the success in the design and implementation of this tool.

From the results found in the different publications, it is noticeable that the great advantage of the design and implementation of the BSC is to contribute to the improvement of the performance of Hospital Units.

Regarding the difficulties/limitations in the design and implementation of this tool, those that are most frequently mentioned are related to access to information, lack of collaboration with researchers, scarcity of human resources, and difficulties related to data (the way of data collection, timing, form of analysis). It is important to identify these limitations/difficulties as a way to overcome them in future investigations.

From the literature found, it is clear the importance that this tool assumes and it is understood that, increasingly, its positive impact at the level of organizations is recognized.

Investigation Limitations

During this literature review, the small number of studies found that met the inclusion criteria, the lack of articles that described the implementation of the BSC in Portugal and that were written in English and the difficulty of accessing to some studies identified as potentially interesting. Another of the limitations felt is related to the fact that not all studies identified indicators for each perspective, nor approach the BSC in the same way, which made the comparative analysis of the different works and the interpretation of data difficult.

Considering the limited time to carry out the study, the search only through the title became necessary, however it proved to be a limitation, and it may have left out some relevant studies.

Research Suggestions

For future investigations, it is suggested that a literature review be carried out with studies carried out in Portugal, in the health area, and that a comparison be made with the results obtained in other countries. Another suggestion is to broaden the inclusion criteria, as well as to review the descriptors, in an attempt to obtain a greater number of studies that allow more generalizations.

Also, according to the analyzed articles, we consider that in future investigations it would be important to apply the BSC complemented with other management tools, to compare the BSC and other performance evaluation methods and to carry out comparative studies between hospitals with the same characteristics in order to understand what factors can influence the application of this tool.

Introduction

According to data from the Organization for Economic Cooperation and Development (2015), Portugal spends more on the health sector than most countries, with hospitals responsible for more than half of public expenditure associated with health care (Alves, 2016). The aging of the population, technological advances, the pressure to reduce public expenditure associated with health care and the growing interest of the private and social sector in this area, raise challenges in the sector, making performance management in this area distinct and complex compared to other areas (Joyce, 2003). Consequently, the need to develop strategic and action plans arose, benchmarking gained prominence, and conditions began to be met for the application of the Balanced Scorecard (BSC) (Calhau, 2009).

The BSC emerged in 1992 with the aim of improving performance measurement systems in the private sector, but quickly gained prominence in the public sector (Alkaabi, Chehab & Selim, 2019). In Portugal, it was no different and came to help organizations in the effective measurement of organizational performance and in the implementation of strategies. It is a performance evaluation model that makes it possible to clarify the organization's objectives and the most appropriate indicators to be used, requiring alignment between the service's strategy and the organization's strategy, as well as the involvement of top and middle managers., for the success of the established methodology (Ojah, Malik & Ali, 2019; Freitas, 2015; Macedo, 2014; Pinto, 2013; Jordan, Neves & Rodrigues, 2011; Alvarez, 1999 cited in Santos, 2006;).

According to Al-kaabi, Chehab and Selim (2019), the BSC provides the basis for properly executing the organization's strategy and successfully managing change. For Pinto (2009), its implementation brings significant benefits in improving the performance of public organizations, if there is an alignment between structural changes, strategic priorities and operational efficiency.

This investigation has as main objective to make, through a systematic review of the literature, a diagnosis of the state of the art, regarding the implementation of the BSC in Hospital Units. Using the existing literature on this topic, it is us objective to answer the following questions: What are the characteristics of the publications that report the application of the BSC in hospitals?; What is the motivation for using the BSC?; What are the characteristics of the hospitals where the BSC was implemented?; Who are the actors in the process of designing and implementing the BSC?; What are the perspectives and performance indicators most frequently used in the application of the BSC in hospitals?; What are the facilitating factors in design and implementation?; What are the results obtained with the implementation of the BSC?; What are the difficulties and/or limitations to the implementation of the BSC?; What opportunities exist for future investigations in this area?.

This systematic literature review arises from the need to promote a better understanding of the subject under study, based on scientific evidence. Through a process of search, selection, organization and synthesis of studies on the implementation of this tool in Hospital Units, and, from the scientific knowledge extracted from them, it is intended, through a process of reflection, analysis and discussion of its content , contribute to the clarification and understanding of this tool, and what benefits can come from its implementation, thus facilitating its adoption and development, by presenting a summary of what has been studied worldwide. The aspects for which this systematic literature review stands out in relation to the existing ones are related to the fact that it focuses only on Hospital Units,

This investigation is divided into five chapters. In chapter one the introduction is made. In chapter two, we provide a framework for the tool under analysis, where general notions about the BSC will be discussed, namely: concept, objectives, perspectives, cause-effect relationship and strategic map, as well as the application of the BSC in the health sector. In chapter three, the methodology used during the investigation will be discussed. In chapter four we will present, analyze and discuss the results, based on the selected literature. Finally, in chapter five the conclusions, limitations and suggestions for future work will be presented.

The Balanced Scorecard

The application of the concept of strategy, associated with management, gained prominence in the middle of the last century (Banza, 2013; Silva, 2012; Barcellos, 2002). For Andrews (1980, p.46) “strategy is the pattern of objectives, purposes or goals and main policies and plans for achieving them, expressed in such a way as to define what business the company is or should be in and the type of company that it is. or shall be.” Mintzberg (1987, cited in Grant, 2013), argues that strategy cannot be seen as a single, finished concept, and, in this sense, defines the 5P's of strategy: Plan, an ordered and coherent sequence of actions; Pattern, coherence and consistency in behavior and decision making; Positioning, adjustment between capabilities and actions, and competition conditions in the surrounding environment; perspective, the way the company sees the world and wants to act in it; and Ploy, tactics to use to gain an advantage over the competition.

Mintzberg (1994) also argues that strategy should be seen as something that is shared and transversal to the different members of the organization and that is reflected in their actions and/or intentions. Other authors (Santos, 2008; Freire, 1997) add that the strategy essentially involves a set of decisions and actions, in which the main purpose is to add value to the customer, in the long term, thus leading to customer loyalty. same.

For the concept of strategy, two fundamental aspects should still be highlighted: first, the relevance of the direct influence of strategy on the future of organizations and, second, the definition of objectives, means and ways to achieve them, as well as their operationalization. in practice, they only make sense if thought of in an integrated and coherent way (Silva, 2012). Sometimes, the problem lies in a poor execution of the strategy, and not in a bad definition of it, a consequence of a misinterpretation of the intended.

As a result of changes in the environment where organizations are located, it has been necessary to invest in the development of knowledge and skills of human resources, in the development of strategic thinking and in the creation of models that are able to respond to new paradigms (Santos, 2008).

Strategic management can be seen as a plan that integrates from objectives to processes, and which makes the entire organization act with a view to achieving competitive results, and that guarantee its permanence in the market (Madaleno, 2015). For strategic planning to be successful, it is important that there is an alignment between it and tactical-operational planning, taking into account the internal and external conditions of the organization. There must also be a focus on innovation and differentiation, considering the relationship between the organization and the environment, thus allowing it to function as a whole towards the intended results (Pinto, 2009; Prieto, Carvalho & Fischmann, 2009; Marçal, 2008); Vieira, 2008; Oliveira, 2006). It can thus be said that strategic management seeks to mold itself to the organization, being characterized by its flexibility in the face of changes in the environment, thus allowing managers to have a broader view of the organization.

In summary, strategic management is assumed as a continuous and dynamic process of planning, organization, leadership and control, through which organizations define “where they are”, “where they want to go” and how “to get there”, being to such a clearly defined strategy is essential (Marçal, 2008; Santos, 2008). For this, it is necessary to act in accordance with the pre-defined path, but always adjusting to changes in the surrounding environment, with special relevance to customers' preferences/needs.

In the elaboration and implementation of strategic planning, Oliveira (2006) describes four phases: strategic diagnosis, company mission, prescriptive and quantitative instruments, control and evaluation. As the execution of the strategy is at the heart of the creation of value and the growth of the organization, the evaluation of its implementation must be the responsibility of the organization's leaders, and this process must include the review and adjustment of the strategy, as well as the processes that support it. (Marçal, 2008).

For Madaleno (2015), the clear definition of objectives, the adequate unfolding and linking of the strategy with the processes, as well as the control of its implementation through a performance measurement system, are crucial in order to achieve the organization's objectives. Despite its simplicity, there are many internal threats to strategy implementation, which can be classified into three groups: those that act on strategic orientation, those that affect the ability to learn, and those that affect the ability to implement the strategy (Beer & Eisenstat, 2000).

For the implementation of a strategic management model that leads to the organization's success in a constantly changing environment, Santos (2008) defends the need for commitment, dedication and involvement of top management; the promotion of a motivating environment, where participation is privileged, favorable to change, and where everyone is encouraged to contribute; adequacy of training to functions; an effective communication system; definition of deadlines for the development of the process; simplification and flexibility of the process, seeing it as a means and not an end to obtain and sustain competitive advantages.

Some authors argue that this process works better when there are performance indicators, thus ensuring adherence between processes/operations/strategy, because when performance measures exist, these will serve as a basis for analysis and decision-making (Skrinjar, Bosilj-Vuksic & Stemberger, 2008; Oliveira, Costa & Cameira, 2007).

In view of the great transformations that have been experienced in the health sector, both globally (where Portugal is no exception) and, considering the current economic and financial scenario, it has been necessary to resort to strategic management instruments in order to help organizations to assess their performance, using different approaches, methodologies, instruments and intervention levels, among which the Balanced Scorecard stands out (Serrano, 2017; Russo, 2015).

Fundamental Elements of the Balanced Scorecard

Performance management is defined by Pinto (2009: 30) “as an integrated system, composed of a set of processes, methodologies and solutions”. This concept has been around for many years and is part of the measurement system, where tools allow us to assess, monitor and review performance. The main objective of performance management is to motivate and align the organization with a view to achieving its mission, vision and strategic objectives, thus achieving better results (Freitas, 2015).

A performance measurement system can be defined as a set of metrics, composed of several elements, which are used to quantify both the efficiency and effectiveness of actions (Neely, Gregory & Platts, 1995). Efficiency refers to the economic use of resources and is a prerequisite for measuring an organization's performance, both in financial and non-financial terms (Lindlbauer, Jonas & Vera, 2016). Effectiveness assesses the outcome of a process where customer expectations/needs are or are not met (Neely, Gregory & Platts, 1995).

According to Rahimi et al. (2018), the causal relationship between indicators, evaluation and performance of the health organization is complex and multidimensional. Therefore, in order to have a powerful evaluation system and be successful in improving hospital performance, instead of focusing on a single dimension, it must pay attention to all dimensions of performance. Among the various instruments for evaluating performance, the Tableau de Bord, Performance Prism and Balanced Scorecard stand out. In recent years, in the health area, most organizations have resorted to the BSC to evaluate their performance, which is recognized as an ideal instrument to achieve organizational transformations and evaluate performance at an organizational and individual level,

For Calhau (2009: 8) “this tool fulfills three essential purposes: it is an efficient measurement system, a strategic management model and a mode of communication”. Unlike traditional performance appraisal systems, which are insufficient to understand, predict and control the determinants of organizational success, the BSC bets on valuing intangible assets, of a qualitative nature, such as service quality, satisfaction level and rate. retention of customers and employees, competence and motivation of human resources, capacity for innovation and adaptation, among others (Santos, 2008). Russo (2015) and Silva (2012) also add that traditional management control systems, being based only on financial criteria, only transmit results from the past, which makes the information incompatible with the strategic objectives. Such systems can lead to intangible indicators being ignored, such as, for example, customer and supplier loyalty, product innovation, process quality, motivation and a higher level of technical knowledge of employees, problem response, etc. It is these indicators that increasingly assume a prominent role in the competitiveness of organizations.

The BSC appears for the first time in 1992, developed by Kaplan and Norton, at a time when there was a great discredit for financial measures, and it was necessary to find new methods to measure the performance of companies. After its implementation, the results were visible and it was the beginning of its success (Calhau, 2009; Kaplan & Norton, 2004).

Kaplan and Norton (1997: 25), refer that the BSC translates the “Mission and strategy into objectives and measures, organized through indicators to inform employees about current and future success vectors. By linking the company's desired results with the drivers of those results, executives hope to channel the energies, skills and specific knowledge of people across the company to achieve long-term goals.”

For the operationalization of the BSC, the use of indicators that are related to the strategic objectives of the organization is used (Madaleno, 2015). As mentioned, such indicators are not limited to evaluating only financial aspects, but also measuring and controlling non-financial indicators (Ojah, Malik & Ali, 2019; Tuan, 2020), which are considered fundamental for achieving the objectives of the organization (Prazeres, Lopes & Meira, 2013). The BSC, by focusing on non-financial indicators combined with financial ones, allows the analysis of all factors surrounding the organization that help in its process of adaptation and change in a world of economic globalization, where competition is increasing (Chavan, 2009).; Chow et al., 1998). In the same way, to recognize that non-financial measures are essential to achieve strategic objectives, is to accept that the complementarity between financial and non-financial indicators can be the pillar for an organization's success (Rompho, 2011; Kaplan & Norton, 1996). It also seeks to respond to the criticisms made to traditional strategic measurement systems, which only valued financial aspects, thus proving to be unsuitable for organizations where intellectual capital is prominent and where the ability to adapt to the demands of the surrounding environment is extremely important. for their success (Manica, 2009; Norreklit, 2003; Ahn, 2001; Kaplan & Norton, 1996). it is to accept that the complementarity between financial and non-financial indicators can be the pillar for an organization's success (Rompho, 2011; Kaplan & Norton, 1996). It also seeks to respond to the criticisms made to traditional strategic measurement systems, which only valued financial aspects, thus proving to be unsuitable for organizations where intellectual capital is prominent and where the ability to adapt to the demands of the surrounding environment is extremely important. for their success (Manica, 2009; Norreklit, 2003; Ahn, 2001; Kaplan & Norton, 1996). it is to accept that the complementarity between financial and non-financial indicators can be the pillar for an organization's success (Rompho, 2011; Kaplan & Norton, 1996). It also seeks to respond to the criticisms made to traditional strategic measurement systems, which only valued financial aspects, thus proving to be unsuitable for organizations where intellectual capital is prominent and where the ability to adapt to the demands of the surrounding environment is extremely important. for their success (Manica, 2009; Norreklit, 2003; Ahn, 2001; Kaplan & Norton, 1996).

According to Tuan (2020) and Martins (2015), by recognizing management weaknesses and inaccuracies, the BSC gives us an indication of what companies should measure to "balance" the financial perspective, providing us with feedback regarding the internal processes of the business and external results, with the aim of continuously improving strategic performance and results.

For Rua e Silva (2016) and Kaplan and Norton (1996), as the BSC is a management tool that aims to provide a global and integrated view of the organization's performance, it is important that there is a good communication of the strategy to the entire organization. and its relationship with the critical success factors, as these condition the organization's performance in the medium and long term. Thus, Alvarez et al. (2019) and Barboza (2011) refer that, in order to apply this tool, it is essential that there is an identification of objectives, indicators and goals by perspective, based on the mission and strategic vision.

According to a study carried out on the implementation of the strategy using the BSC, the following principles are identified as best practices with a view to success and achieving tangible benefits (Kaplan & Norton, 2000): mobilizing change through leadership executive; translate the strategy into operational terms; align the organization to the strategy; transform strategy into an everyday task for everyone, and transform strategy into an ongoing process. These authors (Kaplan & Norton, 2006) refer that, among these principles, the one that most facilitates the successful implementation of the strategy is organizational alignment.

It can thus be said that the BSC is a measurement instrument that allows clarifying and translating the organization's vision and strategy, of continuous learning, a communication tool made up of balanced performance indicators that facilitate the alignment between the operational part and the strategic objectives, which allows the monitoring and feedback of actions and practices by the leaders of organizations, and which facilitates the planning and allocation of resources (Tarigan & Bachtiar, 2019; Jordan, Neves & Rodrigues, 2011; Niven, 2002; Malina & Selto , 2001; Epstein & Manzoni, 1998; Kaplan & Norton, 1996). This tool considers the balance between short- and long-term objectives, financial and non-financial indicators, result indicators and inducing indicators, as well as between internal and external performance perspectives.external, thus leading to the achievement of the organization's strategy, increasing its efficiency and effectiveness (Santos, 2008; Kaplan & Norton, 1996).

The BSC uses a strategic map to materialize the organization's vision and strategy. This map includes the objectives, organized according to four different perspectives: financial, customers, internal processes and learning and growth (Freitas, 2015; Calhau, 2009; Kaplan & Norton, 1997). By considering these four perspectives, it allows managers to define which are the most important perspectives and objectives according to the organization's vision and strategy, always bearing in mind that none of them works in isolation or autonomously.

The implementation of the BSC implies: identifying the mission, vision, strategy and critical success factors, selecting indicators, evaluating, creating action plans and monitoring and managing (Kaplan & Norton, 2001). In addition to these processes, the implementation of the BSC implies the definition of a cause-effect relationship between perspectives, strategic objectives and indicators, so that the causal relationship that was assumed when defining the strategy is perceptible (Pinto, 2009). Kaplan and Norton (1996) stated that in order to have a link between the BSC, the organization's policies and strategies, three principles must be respected: interconnection with financial objectives, cause-effect relationships and performance indicators.

After being implemented, it is expected that: the strategy leads to the implementation of corrective actions, the strategic indicators are applied in the organization's processes, a systematized view of organizational performance is provided, a culture of learning and continuous improvement is developed, there is attribution of incentives and the strategy implemented is regularly tested (Kaplan & Norton, 2008).

Thus, the logic of this tool lies in its integrated operation, with the objectives and indicators establishing cause-effect relationships among themselves. In this sense, the objectives placed at the bottom are those that will lead to the achievement of the objectives placed at the top, that is, it is through the chain and the relationships established between them that the organization's strategy is achieved. This model is characterized, therefore, by its flexibility, it can be adjusted according to the organization, being subject to adaptations and refinements (Niven, 2005).

According to Collis and Rukstad (2008), Padoveze (2007), and Kaplan and Norton (1996, 1992), when considered a strategic management tool for management control, it allows informing stakeholders of strategic decisions and actions, and involves all stakeholders, thus facilitating the understanding of the vision and strategy, leading to alignment in all its aspects. When used properly, it plays an extremely important role in communicating organizational strategy to different employees, allowing feedback and linking long-term strategy with short-term actions, while creating strategic awareness among employees. It is in this context that the approach adopted by the BSC will help managers to define the organization's strategy.

Mission, Vision, Values and Strategy

In order to put the organization's strategy into practice and for it to move towards success, it is necessary that there is a clear definition of the organization's mission, vision, values and strategy, using financial and non-financial performance indicators (for example, Dias, 2014; Kaplan & Norton, 2001).

For all these reasons, it is important to clarify these four concepts.

- Mission: defines the organization's raison d'être, its uniqueness, its central purpose and what social function it performs (Hitt, Ireland & Hoskisson, 2009; Kaplan & Norton, 2004; Niven 2003; Tachizawa & Rezende, 2000). It must be clearly defined, it must make sense to the internal public and be understood by the external public, being specific to the organization in question (Dias, 2014). It can be seen, therefore, that it should serve as a guide for stakeholders. It is important to be considered in the implementation of the BSC, as it is the starting point for the strategy. Kaplan and Norton (2004) refer that the mission must define the direction of activities and which values guide these activities, as well as clearly assume the way to compete in the market and add value to customers. An effective mission is, for Pinto (2009),

achieve, involving not only the organization, but all stakeholders. According to Serrano (2017), the definition of the mission assumes greater importance when dealing with public or non-profit organizations. For this author, in private sector organizations, mission is not a central issue, whereas in public and social sector organizations, mission assumes an extremely important role, as they are totally mission-oriented.

- Vision: is a clear, precise and comprehensive statement that reflects the organization's intentions and aspirations, that is, what the organization wants to achieve in the future (Hitt, Ireland & Hoskisson, 2009; Kaplan & Norton, 2004; Niven, 2003; Tachizawa & Rezende, 2000), with the use of resources, products and services that it has or will have (Pinto, 2009). It must be market-oriented, convey how it wants to be perceived by the outside and reflect its values and aspirations (Senge, 2010; Hitt, Ireland & Hoskisson, 2009; Kaplan & Norton, 2004), thus presenting itself as essential for any type of business. organization: public, private, public-private or non-profit (Pinto, 2009). The mission and vision, are the pillars on which top management will rely to start the process of building and implementing the strategy (Serrano, 2017), and the vision should only be formulated after defining the organization’s mission and values (Pinto, 2009). The vision is thus seen as the starting point for the definition of priorities and as one of the fundamental pillars for the construction of programs and strategic maps that will serve as a guiding guide for the organization and that will help it to achieve success (Serrano, 2017).).

- Values: they are principles that guide an organization, portray its beliefs and define the perception of what is important, right and wrong, fair and unfair (Sousa, 2016; Senge, 2010; Niven, 2003) and are interconnected with the mission, allowing them to have a logical continuity (Kaplan & Norton, 2008; Collins & Porras, 1996). According to Sousa (2016) and Werner and Xu (2012), values are the guiding principles of an organization, thus defining how the organization should act in accordance with its mission, while accompanying the organization to achieve your vision.

- Strategy: set of hypotheses, decisions and actions that represent the way forward to reach the desirable future, described in the vision and that allow adding value to stakeholders (Dias, 2014; Kallás & Coutinho, 2005; Kaplan & Norton, 1997). Alves (2016) states that the definition of strategy assumes a special prominence in the BSC and its execution is one of the most difficult tasks of the leaders, being for it is important that there is a clarification of the strategic orientation before the implementation of this tool.

For Pinto (2009), the mission, vision, and values highlight the “why” and “who”, whereas the strategy tells us “How”. After defining and clarifying these concepts, organizations are in a position to prepare and implement the BSC (Dias, 2014).

Objectives, Indicators, Goals and Initiatives

The BSC cannot be seen only as a measurement system, but as a management system (Gallon et al., 2008). As such, it allows organizations to measure and qualify their vision and strategy and translate it into action. As mentioned above, this tool is based on four perspectives (Financial, Customers, Internal Processes and Learning and Growth), each of which has its own strategic objectives. In turn, these objectives will allow the organization to achieve its mission and vision (Kaplan & Norton, 1997).

According to Norreklit (2000) and Mooraj, Oyon and Hostettler (1999), for each of the strategic objectives, indicators are defined, and the choice of these must be made taking into account some criteria, namely: link to the strategy, accessibility and relevance. The same authors state that, in these indicators, cause-effect relationships are a central aspect of the BSC.

When using the BSC, managers have at their disposal four management processes that, alone or together, help to combine long-term goals with short-term goals, namely vision translation, communication and connection, planning of business and feedback and learning (Kaplan & Norton, 1996). These management processes provide the necessary steps to achieve financial success in future terms, based on non-financial indicators (Kaplan & Norton, 1996; Malina & Selto, 2001). For these authors, the achievement of short-term financial goals should not be considered satisfactory when it is expected that long-term measures are not being properly implemented. It is important that managers who use the BSC do not rely only on short-term financial measures. term, as performance indicators, as they give us information about how well the past has worked, but little information about what the future might look like.

The use of this tool only makes sense when the process begins with top management, allowing it to translate the organization's strategy into strategic objectives. For Kallás and Ribeiro (2008), these objectives should be organized in a diagram so that cause-effect relationships can be identified in different perspectives. For Alves (2016), when translating the vision and strategy, the BSC facilitates the definition of actions to be taken to define the strategic map, as well as helping to create consensus among managers of the organization's vision and strategy. According to Padoveze (2007), if there is communication and association between objectives and strategic measures, managers can ensure that all employees understand the long-term strategy, and that everyone's objectives are aligned.

The choice of indicators is an extremely important task, as the wrong choice can lead to wasted investments. After choosing these, they should be reviewed between top management and middle management, which facilitates the evaluation of strategies according to new information that emerges about competitors, customers, markets, technologies and suppliers (Kaplan & Norton, 2004, 1996).

Some authors (Bourguignon, Malleret & Norreklit, 2004; Ittner & Larcker, 1998) argue that, being a flexible system, the BSC facilitates the definition of both the number of indicators and the weight that each one should assume, which can be adjusted by the organization itself. In a study carried out by Inamdar, Kaplan and Bower (2002), in nine health organizations, these authors define that each perspective should ideally have the following weight: clients 33%; internal processes 27%; financial 23%; learning and growth 17%, however, it will be up to each organization to define the weight to be attributed according to its reality and strategy.

For the implementation of the BSC to be successful, as important as the definition of objectives and indicators, is the definition of goals and initiatives (Serrano, 2017):

- Goals: must be clear and concise, stipulated for each of the perspectives and must state what the organization hopes to achieve (Alves, 2016). Your choice should fall on the aspects that lead to an improvement in the organization's performance, as well as the aspects that help it to improve its range of skills (Alves, 2016). According to the same author, each objective has associated goals, and should facilitate the achievement of the organization's strategy. If the objective does not prove useful in consolidating the organization's strategy, it must be eliminated or the strategy must be changed.

- Indicators: help to assess the success of each objective, that is, they facilitate the assessment of the degree of achievement of each objective (Alves, 2016). Indicators should be of two types, lagging indicators and leading indicators. The BSC is stronger the better the mix of indicators used in each of the strategic areas (Norreklit, 2000; Epstein & Manzoni, 1998).

- goals: they define the level of performance or the rate of improvement intended for each of the defined indicators (Alves, 2016) and must be adapted to each of the strategic objectives, based on real estimates, the time needed to produce benefits and the resources available (Caldeira, 2010; Kaplan & Norton, 2009). Its definition must be cautious, so that it can be achieved, as the definition of unrealistic goals can lead to demotivation of professionals (Caldeira, 2010; Kaplan & Norton 2004).

- Initiatives: they are seen as action plans, where the actions that will contribute to achieving established goals are defined (Werner & Xu, 2012). Kaplan and Norton (2009) state that initiatives are the force that drives the organization to fight inertia and resistance to change.

Cause-Effect Relationships and Strategic Map

For Kaplan and Norton (1996), within the BSC, strategy is nothing more than a set of hypotheses about causes and effects, that is, for every action there will be a reaction, with an impact on the organization's business and that will influence the implementation of your strategy(ies). To implement the BSC, it is necessary to establish cause-effect relationships between the four perspectives, between outcome measures and between performance vectors. Pinto (2009) also corroborates this idea. By stating that this tool's fundamental principle is the definition and verification of cause-effect relationships between perspectives, objectives, goals and indicators.

When developing the BSC in for-profit organizations, the focus is on financial objectives, however, in public sector organizations (non-profit) this tool begins with the definition of the organization's mission (Pinto, 2009). This author also states that cause-effect relationships go through the formulation of simple questions that will lead to the definition of objectives and strategies, which in turn will contribute to the correct identification of which competencies and infrastructures the organization needs. bet so that it can support internal processes and, therefore, satisfy customers. Cause-effect relationships allow us to assess the extent to which the BSC portrays the organization's strategy,

For Alvarez et al., (2019) the strategic map is developed by analyzing the cause-effect relationships between the different objectives. It is a graphic relationship, the way in which the objectives are related in one perspective and also the relationship they establish between the other perspectives, constituting what is called alignment of objectives. This alignment makes it possible to clarify that the achievement of some goals leads to the achievement of others (Alvarez et al., 2019).

The strategic map, when adjusted to the organization's strategy, indicates the path to transform intangible assets into tangible assets, that is, it describes how the former lead to performance improvements in internal processes, which in turn translate into in creating value for customers, shareholders and the community. This strategic map is constructed by establishing a vertical vector through the four perspectives and promotes communication within the organization, while constituting a strategic feedback system (Sousa, 2016; Marçal, 2008; Norreklit, 2003; Ahn, 2001; Kaplan & Norton, 2000, 1996; Mooraj, Oyon & Hostettler,

1999).

Cause-effect relationships are used to communicate how employees can contribute to the achievement of established goals, thus implying that there is a clear link with the implementation of the strategy. Cause-effect relationships also facilitate understanding regarding the allocation of resources and capabilities (Caudle, 2008; Ahn, 2001). In turn, the strategic map creates the foundation for the implementation of strategies quickly and effectively (Kaplan & Norton, 2001), and can be seen as the structure that is used to communicate the history of the strategy to the target audience (Alves, 2016). And helping organizations to see their strategies in a coherent, integrated and systematic way (Quintella, 2004).

This framework clarifies the organization's strategy and values, making it easier for employees to understand how their activities can contribute to the organization's success. This understanding on the part of everyone is essential for the implementation of the strategy to be successful (Barbosa & Perez, 2016; Madaleno, 2015; Maia, Oliveira & Martins, 2008; Atkinson, 2006; Niven, 2005). Smith (2007) states that strategic maps are a great means of communication, as they indicate which are the most critical processes and what positive impact would be obtained in financial terms and on customer satisfaction if improvements were made to them.

For Sousa and Rodrigues (2002), the strategic map must translate the organization's strategy into operational terms, as well as being a facilitating element for the evaluation of performance.

According to Kaplan and Norton (2001), it is in the strategic map that the essential objectives are explained, as well as the links that define the organization's strategy. Among these, the following stand out:

-Objectives to increase shareholder value;

- Market share, acquisition and retention of target customers;

- Value proposition that contributes to a higher profit margin;

- Innovation and excellence in products, services and processes;

- Necessary investments in human and technological resources to generate and maintain growth.

The strategy map is built from top to bottom, improves clarity and focus, as well as represents the missing link between strategy formulation and execution (Kaplan & Norton, 2004). According to Penha and Costa (2012), the strategic map includes four stages: definition of the strategy; identification of essential perspectives for the development of the strategy; definition of the strategic objectives to be achieved in each perspective, and finally representation of the cause-and-effect relationship between the perspectives/objectives.

It is up to each organization to customize its strategy map according to its specific objectives. Kaplan and Norton (2004) argue that organizations can develop and communicate their strategies using approximately two to three dozen objectives, provided that the strategic map is well prepared and clearly identifies the cause-and-effect relationships between them. they.

In 1996, the same authors stated that the BSC is based on the global vision of the organizations' strategy, supported by four perspectives, and that for each of them objectives and indicators are defined that need to work in an integrated and balanced way. For Norreklit (2000), it is these relationships that distinguish the BSC from other strategic management systems. A failure to achieve the objectives of one perspective will lead to efficiency drops in the other perspectives, thus causing an imbalance in the BSC, and negatively affecting the implementation of the strategy, as well as the fulfilment of the organization's mission and vision. That said, it is clear that the strategic maps are the basis for the construction of the BSC.

prospects

The BSC is based on the organization's strategic vision and is supported by four perspectives: financial, customers, processes and learning. For each of these perspectives, objectives and indicators are stipulated, which act in an integrated manner and establish, among the four perspectives, cause-effect relationships (Serrano, 2017; Sousa, 2016; Alves, 2016; Dias, 2014; Kaplan & Norton, 1996).

It is thus clear that this tool does not only include financial indicators, but also non-financial indicators, and it is with the use of these indicators of a non-financial nature that manages to achieve its objective of measuring the performance of the organization (Dias, 2014; Corral & Urieta, 2001). Pinto (2009) draws attention to the fact that this tool makes it possible to establish a link between short-term objectives and the long-term strategy, which is one of the aspects that puts him at the forefront in terms of management systems. performance measurement.

Kaplan and Norton (1997) state that short and long-term objectives, results and performance vectors should be defined having as a reference point the performance measurement of the four perspectives and, given that the BSC is a tool for systemic nature, these objectives must be clearly and balanced, which is the level of integration of the organization's strategy, thus avoiding that the focus is only on one of the perspectives.

It only makes sense to think about these perspectives, when the organization's vision and strategy are placed at the center of them. Pinto (2009) complements this theory and states that vision and strategy are not only the starting point, but also the light that should direct the way, with a view to achieving the organization's long-term goals.

For each of the perspectives, there are defined questions, which indicate what should be measured in each of them (Kaplan & Norton, 1996, 1992):

- Financial: To be financially successful, how should we present ourselves to shareholders?

- Clients: To achieve our vision, how should we present ourselves to our clients?

- Internal Processes: To satisfy customers and shareholders, what processes must we excel at?

- Learning and Growth: To achieve our vision, will we continually be able to change and improve?

Financial Perspective: for a long time, financial indicators were considered the only way to measure an organization's performance. The BSC seeks to go further and consider the interaction between this perspective and the others, thus, allowing managers to identify in which perspectives they should act at a given moment to achieve financial goals.

According to Serrano (2017), this perspective represents the most traditional way of evaluating results, and it is the one that is most used to evaluate the results of organizational performance, it is closely related to the interests of shareholders, which are mainly of financial character.

The financial perspective considers the balance between short and long-term objectives, and for many organizations it occupies the top of the strategic map (Kaplan & Norton, 2001, 1993, 1992), especially in private organizations. In the case of public organizations, this can appear either at the top of the strategic map next to the customers' perspective, or in second place, immediately before the customers' perspective.

For Kaplan and Norton (1997), financial objectives and indicators play a dual role. If, on the one hand, they define the expected financial performance of the strategy, on the other hand, they serve as a reference for the objectives and indicators of all other perspectives.

According to Ferreira (2012), the isolated use of economic and financial indicators can harm the creation of long-term value, as it tends to focus attention on short-term results. The importance of all the objectives and indicators of the remaining perspectives being linked to the objectives of this perspective is highlighted, orienting towards long-term goals, while ensuring that all strategies and initiatives are directed towards achieving the financial objectives. Financial indicators are different depending on the life cycle of the organization, the most used being the rate of return, cost reduction rate, growth and sales volume, percentage of investment, return on investment, net income for the period, among others (Zhou et al., 2020; Jordan, Neves & Rodrigues, 2011; Kaplan & Norton, 2001; Lipe & Palter, 2000).

When it comes to public and non-profit hospitals, Dias (2014) states that the objective is not the return of shareholders, as such, the fundamental thing is for the organization to have financial resources, to know how to monetize them and transform them into benefits for their employees. customers/users. Serrano (2017) reinforces the previous idea and adds that, in the BSC, financial indicators are of great importance in this type of organizations, as the human, material and financial resources are essential for the proper functioning of organizations.

Customers Perspective: many organizations stipulate their mission with customer focus. By assuming this position, the customer perspective becomes the priority of top managers (Dias, 2014; Pinto, 2009; Caudle, 2008; Mooraj, Oyon & Hostettler, 1999; Kaplan & Norton, 1996, 1992). Kaplan and Norton (1996) mention that this concern is important not only in the private sector, but also in the public sector and non-profit organizations.

This perspective translates the mission and strategy into customer-oriented objectives. As such, it is necessary to identify the customer segments and markets where they wish to compete, and that these objectives are communicated to the entire organization (Alves, 2016; Martins, 2015; Russo, 2015; Dias, 2014; Caldeira, 2010; Kaplan & Norton, 1996). Kaplan and Norton (1997) state that when organizations do not understand customer needs, they end up losing them to others where there is greater appreciation of customer needs/preferences.

According to Santos (2008), this perspective is concerned with the way the organization is seen by its customers and with the way it would like to be seen by them. As such, it is concerned with creating value for the customer so that it becomes loyal (Russo, 2015), allowing the alignment of its results indicators related to customers (satisfaction, loyalty, retention, capture) with specific market segments. (Serrano, 2017; Banza, 2013). It is thus understood the importance of finding key indicators adjusted to the organization's strategy, and that help it to understand both customers and their needs. As it is related to customer satisfaction, it is important that all elements of the organization make the relationship and satisfaction of their needs a priority.

Kaplan and Norton (1996, 2000) state that the focus of any strategy is the value proposition for the customer, which is achieved through the combination of a set of aspects, namely products and services, relationship with customers and external image. These authors point out as value propositions: operational excellence; customer intimacy; and product leadership.

Internal Processes Perspective: considers the measures/efforts that the organization makes to improve existing operational processes, in order to meet the expectations of customers, shareholders, as well as achieving the organization's financial objectives. In general, this perspective seeks to achieve what is the quality desired by the customer, without ever forgetting the strategic objectives of the organization (Russo, 2015; Dias, 2014; Werner & Xu, 2012; Caldeira, 2010; Manica, 2009; Matos & Ramos, 2009; Pinto, 2009; Kaplan & Norton, 1996, 1992).

For Martunis et al. (2020), the perspective of internal processes refers to the organization's ability to perform work activities as planned.

Serrano (2017) and Kaplan and Norton (1996) tell us that core processes are those that have the greatest impact on customer satisfaction and that organizations should decide which processes and competencies they should achieve excellence in, as well as how to specify the objectives and indicators for each one of them, in order to achieve competitive advantage. In this way, excellence is achieved through processes, actions and decisions that occur throughout the organization, with innovation processes assuming a leading role towards good financial performance. It is therefore essential that these organizations identify which are the key processes for creating value, in order to improve them.

The perspective of internal processes, with the aim of achieving the strategic objectives of the organization, seeks to find a solution to the following challenges: growth; produce value; deliver the proposed value to customers; value assets; improve processes and reduce production component costs (Serrano, 2017; Santos, 2008). According to Alves (2016) and Dias (2014), cycle time, costs, quality, productivity and innovation are used as main indicators.

Managers must stipulate a value chain of internal processes that must focus on three major areas: innovation, operations and after-sales (Kaplan & Norton, 1997). By carrying out measurements from this perspective, managers can better understand and know how their business, products and services work. services, according to the customer's requirements. The better the managers know the process, the better the adequacy of the strategies.

Learning and Growth Perspective: from this perspective, the main sources are: people, systems and procedures (Russo, 2015; Kaplan & Norton, 1996). The BSC emphasizes the importance of investing in learning, always with an eye on the future, and considering that in order to face technological changes it is necessary to invest in continuous learning (Massingham, Massingham & Dumay, 2018; Martins, 2015; Dias, 2014) so that the organization can grow and develop in the medium/long term (Alves, 2016). For Martunis et al. (2020), this perspective represents the organization's effort to improve the quality of the performance of its human resources.

It is in this perspective that the main competencies and skills, technologies, values and culture necessary, which support the organization's strategy and where priorities are defined that help in the construction of an organizational environment that supports innovation, growth and change (Dias, 2014; Kaplan & Norton, 2004, 2001, 1996).

According to Kaplan and Norton (2004, 1996), this perspective considers a series of intangible values, such as human capital, information capital and organizational capital, which establish cause-effect relationships with the other perspectives, thus leading to success. end obtained from the top perspective – customer perspective, in the case of the public sector. For this to happen, it is necessary to invest in the retraining of employees, in the development of technologies, and in the alignment of organizational procedures and routines, to fill the gaps between the necessary and existing capabilities (Kaplan & Norton, 2004; Mooraj)., Oyon & Hostettler, 1999).

With regard to the learning and growth perspective, Kaplan and Norton (1997) refer to the needs of the organization, that is, what it needs to develop in order to grow in the long term. As such, this perspective uses indicators such as professional satisfaction, professional training and length of service.

This perspective stands out from the others, because its objectives are defined after identifying the needs in the other perspectives, and thus the one that will be the inducer of the results achieved in the other perspectives, given the interdependence relationship between them (Norreklit, 2003).; Santos, 2008).

For Pinto (2009), this perspective underlines which factors, in terms of resources and infrastructure, in which the organization should invest in order to be competitive, being increasingly important, as it is concerned not only with maintenance, but also with the long-term sustainability of the organization (Alves, 2016). It is essential for the success of the organization that human resources have adequate training, are motivated, involved and aligned, as only then will they lead to success (Kaplan & Norton, 1996).

The BSC gives the manager a view of the business from these four perspectives, in a quantifiable and objective way, avoiding excess information (Dias, 2014; Kanji & Sá', 2002). According to Serrano (2017), the four perspectives are interconnected in a cause-effect relationship, and the vision and the strategy simultaneously represent the pillars and the starting point for the construction and development of the BSC.

Although the literature highlights the importance of the four perspectives, it is important to understand the order stipulated for the different perspectives, depending on the scope of the organization (public, private, public-private and social).

BSC in the Health Sector

The health sector has an enormous impact in terms of economic significance, representing one of the biggest consumers of public resources, at the same time that it is subject to enormous criticism from citizens, given that its function is to prevent disease and treat their health. However, it must always be kept in mind that we live with a scarcity of resources and with virtually unlimited needs, so careful decision-making is extremely important when it comes to the use of resources. In this context, the use of the BSC represents a valuable tool in the management of organizations operating in the health sector, given its characteristics of complexity and high degree of uncertainty (Inamdar, Kaplan & Bower, (2002). Zelman, Pink and Matthias (2003) also state that the use of the BSC is extremely important for the hospital environment, as it allows establishing a link between practice, quality, results, value and costs. Other authors also argue that by using this tool it is easier to achieve alignment between organizational strategy, action plans and performance management, as there will be a union between vision, values and day-to-day operations (Carvalho, Dias & Prochnik, 2005).

The use of the BSC in healthcare for the first time was Griffith's responsibility in 1994. Since then, its use in this field has gained prominence. According to Inamdar, Kaplan and Bower (2002), the use of the BSC in this area represents a valuable tool in the management of organizations operating in the health sector, given its characteristics of complexity and high degree of uncertainty.

Silva and Prochnik (2005) and Baraldi (2002) point out as the main aspects that underlie the use of this tool in health organizations, the following:

- Difficulty linking indicators to strategic planning;

- Problematic information systems;

- Lack of formal measurement systems;

- Deficit of coordination between health professionals and administrators;

- Wide range of consumer needs;

- Greater competitiveness.

Several factors boosted the use of the BSC in hospital institutions, including strong economic and financial pressures related to rising health care costs, political pressures to contain public expenditure, and technological advances. All these aspects led managers to implement management tools, which until then were developed in the private sector, but with proven evidence that they led to increased performance when associated with an efficient management of resources (Quesado & Macedo, 2010). As a result of growing budgetary constraints in this area, the introduction of management systems becomes increasingly important, as it facilitates monitoring, evaluation, and decision-making support with a view to improving the performance of organizations. As management systems are traditionally applied in the private context, Tarigan and Bachtiar (2019) and Niven (2005) report that more and more public hospitals use the BSC, and have managed to obtain attractive results, as it allows them to find ways to articulate your strategies, and quantify your success with regard to achieving goals.

Santos (2008) mentions that the successful implementation of the model is laborious and must come from the top management, which is the one who prepares the policies and is responsible for their execution. In the health area, the use of this tool must include the use of indicators of structure, processes, results and those related to the external environment or environment. Through this set of indicators, it is possible to obtain information with the objective of achieving efficiency and effectiveness (Bittar, 2001). Kaplan and Norton (2001) refer that to implement the BSC in health it is necessary to: mobilize change through executive leadership, translate the strategy into operational terms, align the organization with the strategy, transform the strategy into a task for all, and convert strategy in an ongoing process.

Although the strategy is the focal point of the BSC, public organizations find it difficult to outline it clearly and concisely. For Kaplan and Norton (2001), this must encompass the organization's mission, it must be visible to everyone, allowing them to understand its purpose.

Although it was created to be implemented in private institutions, some changes are necessary when implementing it in the public sector. Several authors state that, contrary to the private sector, public organizations do not present the financial perspective as a final objective, and as such, the perspective placed at the top is the Customer perspective (Tarigan & Bachtiar, 2019; Kaplan, 2010; Caldeira, 2010; Matos & Ramos, 2009; Pinto, 2009; Kaplan & Norton, 1997; Niven, 2005). In public organizations, financial objectives will be seen as a facilitating or restrictive element towards customer satisfaction (Alves, 2016; Niven, 2005).

- Mission – appears at the top of the BSC and works as a fifth perspective. In public hospitals, the Mission should be more comprehensive and towards which the objectives, goals and initiatives stipulated for the other perspectives must converge (Dias, 2014; Tarigan and Bachtiar, 2019).

- Customer Perspective – assumes the main role, right after the mission.

- Financial Perspective – it is no longer at the top and comes before the customers, meaning that it is a resource and, at the same time, a constraint associated with the existing budgetary rules in the sector.

The adoption of the BSC in many world health organizations has led them to success, as it is used as a tool that helps in the control of management and allows a better assessment of their efficiency and effectiveness (Ribeiro, 2008). Thus, this tool, when applied to health, does not represent just a simple instrument of measurement and control, but an evolution in terms of strategic management. The successful implementation of the BSC has been considered an asset at the level of health organizations, as it helps to improve the performance of the hospital, as well as the national health system (Ba-Abaad, 2009). Zelman, Pink and Matthias (2003) also state that the use of the BSC is extremely important for the hospital environment, as it allows establishing a link between practice, quality, results, value and costs.

There are several successful cases reported, of which the following stand out:

- According to data published at Duke Children's Hospital, in the United States, the BSC began to be used in 1996, and in 2000, user satisfaction had already improved by 18%, professional satisfaction by 45%, the average patient stay went from 7, 9 to 6.1 days, the readmission rate from 7 to 3%, and the cost per patient decreased by about

5,000 dollars (Meliones, 2000). These changes made the hospital, which was in a situation of loss, start to make a profit (Meliones, 2000).

- Another example, which demonstrates the good results obtained with the application of the BSC, is the case of a Thai hospital that applied this tool in the emergency department and found that: the levels of satisfaction of its employees increased; there were improvements in the performance time of the laboratories, which in turn led to improvements in patient care, in turn increasing service satisfaction; in operational terms positive results were obtained; and that investment in training, in the areas of customer service and communication, contributed to increased user satisfaction (Matos & Ramos, 2009).

- Hospital Nove de Julho, in São Paulo, one of the first to implement the BSC in Brazil, also recorded positive results after using this tool, having already received awards for quality and customer service (Alves, 2016).

- At Mackay Memorial Hospital in Taiwan, the BSC was implemented in 2001, with the aim of increasing the hospital's competitive advantage. According to Chang et al. (2008), the implementation of this tool contributed to learning and continuous improvement, allowing the administration to improve the view on the industry, as well as on the competitive position of the hospital. With the results achieved after the implementation, this hospital was able to reinforce its competitive advantage (Chang et al., 2008).

In Portugal, although the importance of performance evaluation is recognized, it is still at an embryonic stage (Pinto, 2009) and the dissemination and study of the BSC is not as advanced as in other European and North American countries (Russo, 2009). 2015). However, Calhau (2009) and Matos (2006), refer that, when implemented, there is a great acceptance by health professionals in the implementation of this tool in Portuguese hospitals, representing the BSC a means to improve the efficiency and effectiveness of same. Management based on the BSC can lead to a more efficient use of public resources, the satisfaction of social needs and the balance between the State's obligations towards taxpayers (Russo, 2015). Serrano (2017), refers that also in Portugal there have been cases of success with the implementation of the BSC in the health sector. For this author, success stories should be used and replicated in different health organizations, provided they are adapted accordingly. By assuming this policy, we would move towards a greater approximation of the different professional classes in the achievement of common goals, improvement in organizational communication, improvement of the quality of the service provided to the user and in the creation of value for them.

Benefits and Difficulties in Applying the BSC Applied to Health Organizations

Reviewing the existing literature on this tool (e.g., Oyewo, Oyedokun & Azuh, 2019; Cruz, Geada & Silva, 2012; Silva & Nunes, 2007; Matos, 2006; Walker & Dunn, 2006; Pereira, 2005; Inamdar, Kaplan & Bower, 2002; Sanchez, Stadnick & Erdmann, 2002) the following benefits achieved with the use of the BSC by health organizations are pointed out:

- It helps to clarify and reach consensus on the strategy;

- Improves the alignment of all professionals around a user-centered strategy, making the strategy a continuous process and a function of all;

- Clarifies the allocation of responsibilities for hospital performance;

- Contributes to the simplification, monitoring and evaluation of the implementation of strategic objectives;

- Increases the credibility of management bodies;

- Facilitates the decision-making process;

- Establishes the essential principles and processes for the implementation of the strategy;

- Optimizes resource allocation;

- Allows you to have a financial and non-financial view of the organization;

- Increases employee motivation;

- Contributes to staff development and retention;

- It allows the development of an information measurement and reporting system, which helps in evaluating the progress and success of the strategy;

- Allows the creation of a communication and collaboration mechanism between professionals;

- Encourages continuous improvement and learning;

- It favors the development of new products;

- It makes management more efficient and systematic;

- Contributes to the improvement of medical care;

- Improves internal processes;

- Allows the maintenance of financial stability;

- It contributes to the reduction of costs, without this having an impact on the quality of the service provided.

Despite all the listed benefits associated with using the BSC, it is also possible that its implementation will not be successful, which may be due to the lack of commitment by top management, little involvement by professionals, too long development processes, recourse to inexperienced consultants and implementation for remuneration purposes (Kaplan & Norton, 2000). Given that these difficulties are felt in other sectors, it is not expected that the situation will be different in the health sector (Carvalho, Dias & Prochnik, 2005).

The problems, described in the literature (eg García, 2007; Silva & Nunes, 2007; Matos, 2006; Carvalho, Dias & Prochnik, 2005; Cruz, 2005; Silva & Prochnik, 2005; Zelman, Pink & Matthias, 2003) associated with the use of the BSC in health can be divided between internal and external, of which some stand out:

- Conflict of interest between administration and clinicians;

- Deficit in the dissemination of performance evaluation methods;

- Ignorance of the BSC;

- Lack of commitment from top management;

- Inexperience in the use/monitoring and evaluation of indicators;

- Difficulty justifying the money invested;

- Difficulty in grouping and selecting the large number of indicators from different sources of information;

- Failure to select performance evaluation indicators.

Although it has limitations, it is important to emphasize that the BSC proves to be a great tool to be used in the public sector. In order to contribute to the improvement of the performance of health organizations, this tool needs, however, to be implemented in a thoughtful and organized way. The success of its implementation depends on effective guidance, monitoring and evaluation (El-Jardali, Saleh & Jamal, 2011).

A recent literature review (Aryani & Setiawan, 2020) led to three fundamental conclusions: that the BSC is widely used, contributing both to the improvement of organizational performance and to the development of the organization's strategy; the Balanced Scorecard implementation status reveals a high level of success, and a low level of failure; although it has limitations, the benefits obtained with its implementation outweigh the limitations and reinforces the view that the BSC is a valid tool to consider in terms of performance management.

However, there are many studies that highlight the non-generalization of its use, the result of a set of barriers that can prevent or limit the chances of success (Quesado, Guzmán and Rodrigues, 2018). For this reason, several authors (Tarigan & Bachtiar, 2019; Gao et al., 2018; Quesado, Guzmán & Rodrigues, 2018; Madsen & Stenheim, 2015; Lueg, 2015; Hoque, 2014; Lueg & Julner, 2014; Lin et al. al., 2013; Lueg & Silva, 2013), refer to the need to develop more studies in this area of knowledge.

The literature review carried out shows that empirical research on this topic is still not enough, and the results obtained are often inconsistent. Although there are already some literature reviews on this topic, they focus essentially on the success or failure in the implementation of the BSC. It is therefore essential to review the literature that, in a systematic way, can clarify and standardize the process of implementing the BSC in the health sector in its different contexts (ie public, private, public-private and social sectors). It is here that this research intends to make its contribution, by identifying and systematizing which indicators are most used worldwide, in each of the perspectives, thus facilitating the most appropriate choice for each reality.

It is in this sense that it seems important to us to answer some questions, namely: What are the characteristics of the publications that report the application of the BSC in hospitals?; What is the motivation for using the BSC?; What are the characteristics of the hospitals where the BSC was implemented?; Who are the actors in the process of designing and implementing the BSC?; What are the perspectives and performance indicators most frequently used in the application of the BSC in hospitals?; What are the facilitating factors in design and implementation?; What are the results obtained with the implementation of the BSC?; What are the difficulties and/or limitations to the implementation of the BSC?; What opportunities are there for future investigations in this area?

Using a literature review as a methodology, we intend to obtain the answer to these questions, present an overview of the existing literature on the application of the BSC in Hospital Units, and summarize the main indicators used in the application of this tool, as well as the main results obtained with its implementation and possible gaps in this area of knowledge. The achievement of these objectives may facilitate the adoption and development of this tool in health institutions, by presenting a summary of what has been studied worldwide.

Methodology

In this chapter, the methodology used in this investigation will be discussed, in order to obtain theoretical support, regarding the research strategy and the procedures adopted for its realization.